IHM NOTES-SEMESTER IV-HOTEL ACCOUNTANCY

UNIFORM SYSTEM OF ACCOUNTS FOR HOTELS

Introduction to Uniform system of accounts

- Regardless of the business size, Accounting in the perspective of Hotel Industry is all about recording and retrieving in & out cash-flow.

- Hotel Accounting is considered as the boon for better decision making that brings in good fortune to hoteliers if handled efficiently.

- Beyond that it involves summarizing, reporting and analyzing the hotel’s financial position for a particular period, further helps in budgeting, forecasting and future cost planning.

- In general, a Certified Public Accountant (CPA), accountant or a bookkeeper takes care of handling the accounting activities and generates the financial statements such as Balance Sheet, Profit & Loss (Income) and Cash Flow, etc.

- And, these are the most crucial components that communicate the financial information of an individual hotel or group of hotels.

- Staying accountable doesn’t end here! Hotel Accounting also involves in keeping the bank account in sync, streamlining the payables & receivables, analyzing

- department- wise expenses, generating general ledger, tracking inventory supplies and 1099 payment reports.

- In terms of Operations front, the accounting plays a key role in Tracking Bills, Recurring Dues, Sales & Journals Approval, while keeping a tab on Occupancy %, Rooms Sold, Average Daily Rate (ADR), RevPar, Room Revenue and Guest Satisfaction Surveys, Competition Analysis through STR, Variance Analysis, Labor Management, Operating Budgets and Financial Benchmarking.

- On the other side, the Time & Payroll Management, Daily Activity Tracking, Performance Monitoring, Daily Sales, Profitability Forecast fall in the lineup of Accounting in Hotel Industry.

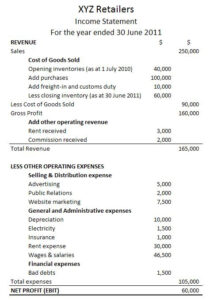

Contents of the Income Statement

The income statement is a financial statement that is used to help determine the past financial performance of the enterprise, predict future performance, and assess the capability of generating future cash flows. It is also known as the profit and loss statement (P&L), statement of operations, or statement of earnings.

The income statement consists of revenues (money received from the sale of products and services, before expenses are taken out, also known as the “top line”) and expenses, along with the resulting net income or loss over a period of time due to earning activities. Net income (the “bottom line”) is the result after all revenues and expenses have been accounted for. The income statement reflects a company’s performance over a period of time. This is in contrast to the balance sheet, which represents a single moment in time.

Contents of the Balance Sheet (under uniform system)

The balance sheet contains statements of assets, liabilities, and shareholders’ equity.

Assets represent things of value that a company owns and has in its possession, or something that will be received and can be measured objectively. They are also called the resources of the business, some examples of assets include receivables, equipment, property and inventory. Assets have value because a business can use or exchange them to produce the services or products of the business.

Liabilities are the debts owed by a business to others–creditors, suppliers, tax authorities, employees, etc. They are obligations that must be paid under certain conditions and time frames. A business incurs many of its liabilities by purchasing items on credit to fund the business operations.

A company’s equity represents retained earnings and funds contributed by its owners or shareholders (capital), who accept the uncertainty that comes with ownership risk in exchange for what they hope will be a good return on their investment.

Fundamental Relationship

The relationship of these items is expressed in the fundamental balance sheet equation:

Assets = Liabilities + Equity

The meaning of this equation is important. Generally, sales growth, whether rapid or slow, dictates a larger asset base – higher levels of inventory, receivables, and fixed assets (plant, property, and equipment). As a company’s assets grow, its liabilities and/or equity also tends to grow in order for its financial position to stay in balance. How assets are supported, or financed, by a corresponding growth in payables, debt liabilities, and equity reveals a lot about a company’s financial health.

Uses of the Balance Sheet

The balance sheet of a business provides a snapshot of its financial status at a particular point in time.

Departmental Income Statements and Expense statements (Schedules 1 to 16)

A Departmental Income Statement shows each departments contribution margin and net income from operating, after all expenses are allocated for. The Departmental Income Statement shows which departments of the company are the most profitable, and which departments are costing the company money

Normally, all direct expenses are charged to the respective departments, in case of indirect or general expenses, proper allocation among the departments must be made in order to ascertain the profit and loss made by each department. Each department is charged with proper business expenses.

INTERNAL CONTROL

Definition and objectives of Internal Control

Internal Control can be defined as a system designed, introduced and maintained by the company’s management and top-level executives, to provide a substantial degree of assurance in achieving business objective, while complying with the policies and laws, safeguarding the assets, maintaining efficiency and effectiveness in regular operations and reliability of financial statements.

Objectives of Internal Control System

- To ensure that the business transactions take place as per the general and specific authorisation of the management.

- To make sure that there is a sequential and systematic recording of every transaction, with the accurate amount in their respective account and in the accounting period in which they take place. It confirms that the financial statement fulfils the relevant statutory requirements.

- To provide security to the company’s assets from unauthorised use. For this purpose, physical security systems are used to provide protection such as security guards, anti-theft devices, surveillance cameras, etc.

- To compare the assets in the record with that of the existing ones at regular intervals and report to the those charged with governance (TCWG), in case any difference is found.

- To evaluate the system of accounting for complete authorisation of the transactions.

- To review the working of the organization and the loopholes in the operations and take necessary steps for its correction.

- To ensure there is the optimum utilization of the firm’s resources, i.e. men, material, machine and money.

- To find out whether the financial statements are in alignment with the accounting concepts and principles.

- An ideal internal control system of an organization is one that ensures best possible utilization of the resources, and that too for the intended use and helps to mitigate the risk involved in it concerning the wastage of organization’s funds and other resources

Characteristics of Internal Control

(CROSSASIA)

- Competent and trustworthy personnel

- Records, Financial and other Organization plan

- Organizational plans

- Segregation of duties

- Supervision

- Authorization

- Sound practice

- Internal Audit

- Arithmetic and accounting controls

Implementation and Review of Internal Control

- Cash− Here, internal control is applied over payments and receipts of an organization. This is to safeguard from misappropriation of cash.

- Control over Sale and Purchase− With proper and efficient control system for transactions regarding purchase and sale of material, handling of material and accounting for the same is must.

- Financial Control− It deals with the efficient system of accounting, recording and supervision.

- Employee’s Remuneration− Internal control system is applied to preparation and maintenance of records of employees and the payment methods also. It is also necessary to safeguard against misappropriation of cash.

- Capital Expenditure− Internal control system ensures the proper sanction of capital expenditure and also the use of it for the purpose intended.

- Inventory Control− It covers the proper handling of inventory, minimization of slow moving items or dead stock, proper valuation of stock, recording of it, etc.

- Control over Investments− internal control system is applied to the proper recording of transactions be it purchases, additions, sale or redemption, income on investments, profit or loss on investment.

Review of Internal Control System

- Internal control system should be reviewed by the Auditor before star audit as described below −

- Reviewing the system of accounting entries, whether recorded as per accounting standard or not.

- To frame audit program according to present circumstances.

- Frauds, errors and mistakes are likely to be located or not.

- To review existence of internal audit program and to check the efficiency of internal control system.

- To review the reliability of reports, records and certificates as presented by the management.

- To check if there is any possibility of improvement in existing internal control system.

INTERNAL AUDIT AND STATUTORY AUDIT

An introduction to Internal and Statutory Audit

Internal audit is a function that, even though operating independently from other departments and involves reporting directly to the audit committee, remains within an organization i.e. the company’s employees. Internal audits involve performing audits of both financial and non-financial nature within a wide of areas of operation in business, including those that are directed by the annual audit plan.

Statutory audit is an audit by a practising Chartered Accountant which has its operations exterior to the organization which it is auditing. Statutory Auditors are a part of the external audit process. Statutory auditors are focused on the various financial accounts or risks associated with the domain of finance and are appointed by the shareholders of the company.

Distinction between Internal Audit and Statutory Audit

- The internal audit is limited to the governance of an organization, management controls over the operations of an organization and risk management. The external audit is related to the reports on financial statements of the corporate entity.

- The external audit is a legal requirement while the internal audit is conducted based on the personal resolve of the business owners to measure the operation’ efficiency as conducted by the business.

- The external audit is performed by an external auditor or audit firm while the process of internal audit is performed by the firm’s employees, nevertheless, an audit firm can also be selected and appointed to conduct the process of internal audit.

- The internal auditor is selected or appointed by the company while the selection of the external auditor is at the shareholder’s annual general meeting.

- The external audit is performed while maintaining in perspective the various requirements of any acceptable financial reporting standards while no such rules hold for internal audit.

- The internal auditor by means of the internal audit process is responsible to report to the management or audit committee while statutory auditor as part of the statutory audit process reports to the company shareholders.

Implementation and Review of internal audit

Control policies and procedures must be established and executed to help ensure that management directives are carried out. They help ensure that necessary actions are taken to address risks to achievement of the organization’s objectives. Control activities occur throughout the organization, at all levels and in all functions. They include a range of activities as diverse as approvals, authorizations, verifications, reconciliations, reviews of operating performance, security of assets and segregation of duties.

Review each cycle to determine whether existing controls are sufficient to avoid potential problems.

Identify any outside policies or procedures in place to offset potential risks.

If controls do not exist or appear ineffective, establish new controls.

Identify any controls that are excessive or unnecessary and modify or eliminate them.

Remember that a good control environment is the first step toward establishing effective controls.

DEPARTMENTAL ACCOUNTING

An introduction to departmental accounting

Departmental Accounting refers to maintaining accounts for one or more branches or departments of the company. Revenues and expenses of the department are recorded and reported separately. The departmental accounts are then consolidated into accounts of the head office to prepare financial statements of the company

Allocation and apportionment of expenses

Allocation and apportionment of overheads. This is also known as departmentalization or primary distribution of overheads.

Allocation of Expenses: Allocation is the process of identification of overheads with cost centres. An expense which is directly identifiable with a specific cost centre is allocated to that centre. So it is the allotment of whole item of cost to a cost centre or cost unit or refers to the charging of expenses which can be identified wholly with a particular department. For example, the whole of overtime wages paid to the workers relating to a particular department should be charged to that department. So, the term allocation means the allotment of the whole item without division to a particular department or cost centre.

Apportionment of Expenses: Cost apportionment is the allotment of proportions of items to cost centers or cost units on an equitable basis. The term refers to the allotment of expenses which cannot identify wholly with a particular department. Such expenses require division and apportionment over two or more cost centers or units. So cost apportionment will arise in case of expenses common to more than one cost centre or unit. It is defined as the allotment to two or more cost centers of proportions of the common items of cost on the estimated basis of benefit received. Common items of overheads are rent and rates, depreciation, repairs and maintenance, lighting, works manager’s salary etc

Advantages of allocation

Support and Operating Centers

To use the direct cost method, first divide your company’s departments into operating and support departments. Operating departments are business functions that directly work toward production. For example, a beverage company may have bottling and mixing operating departments. Support departments provide services to other departments

Allocation Ease

Direct method costing only allocates costs from support departments to production departments. This can greatly reduce the number of allocations that you have to make. For example, if your company has four support departments and two production departments, you will make eight allocation calculations using the direct costing method.

Focus on Production

Because support center costs are only allocated to operating departments, you focus costs of supporting the business toward production. While this may not be the most accurate method of allocating costs, it has a strong theoretical basis. If not for the production departments, the support centers would not be needed

Accuracy Disadvantages

The primary disadvantage of the direct costing method is accuracy. Because support departments’ costs are not allocated to other support departments, businesses systematically over-allocate production departments’ costs and under-allocates support departments’ costs. The extent of this inaccuracy depends on the amount of resources the production departments use compared to the support departments

Draw-backs of allocation

The departmental overhead rate will skew when each department is responsible for multiple products varying in labor and machine hours. This is likely to occur when departments are large. This also creates redundancy since each department must measure and calculate its respective rate. Departmental overhead rates assume that costs can easily be separated from one department to another.

Basis of allocation

An allocation base is the basis upon which an entity allocates its overhead costs. An allocation base takes the form of a quantity, such as machine hours used, kilowatt hours consumed, or square footage occupied. Cost allocations are mostly used to assign overhead costs to produced inventory, as required by several accounting frameworks.